The independent resource on global security

4. Arms production and military services

Contents

Summary

The economic downturn following the 2008 global financial crisis and the subsequent austerity measures imposed in North America and Western Europe began to have an impact on sales in the world’s arms industry in 2011–12. However, the impact on the industry was not uniform, with varied results for individual company.

Ongoing spending discussions have generated uncertainty in the largest arms and military services market—the United States—and are a key reason companies based there and in Western Europe are seeking increased market shares in other regions, including Asia, Latin America and the Middle East. Individual companies are taking steps to insulate themselves against austerity measures through military specialization, downsizing, diversification, and exports and other forms of internationalization. In some cases company subsidiaries have maintained or increased arms and military services sales outside of the countries in which the parent companies are headquartered.

Companies also use acquisitions to improve the products and services they already deliver. While much attention is paid to acquisitions, a number of divestitures also indicate the ways in which the industry is restructuring to accommodate the austerity environment and changing customer requirements.

Governments use a number of strategies to assist their arms industries outside of their home markets. These include direct government arms export promotion; support for cost reductions; and the use of rhetoric about arms industry employment. In contrast, countries that have not cut military expenditure see this dilemma as an opportunity to either obtain more favourable terms on arms imports or to develop their own industries.

Cybersecurity and the arms industry

The growing importance of cybersecurity in the military and civil realms has led to noteworthy diversification by arms-production and military services companies into the cybersecurity

market.

In 2012 cybersecurity continued to rise on the agendas of the international political and security communities. Revelations about Flames and Stuxnet made headlines and inspired fresh discussions about the growing use of cyberweapons and cyberwarfare. While there is no reliable evidence, a growing number of countries—including China, Iran, Israel, Russia and the USA—were suspected of using cyberweapons and making offensive interventions across cyberspace.

The rise of cybersecurity on the political and military agenda has evident economic implications. According to one estimate, global public and private cybersecurity spending was approximately $60 billion in 2011 (equal to 3.5 per cent of world military expenditure). The USA was the biggest spender on cybersecurity, accounting for half of the total, and was the only country where the levels of public and private spending on cybersecurity were almost equal. In the rest of the world, the private sector accounted for the majority of national spending on cybersecurity.

States’ reliance on private cybersecurity providers could become a matter of political concern, particularly with regard to democratic transparency, oversight, accountability and cost. The provision of services by arms-producing companies—as well as traditional cybersecurity providers—may change the way in which states define and manage their cybersecurity and cyberdefence policies.

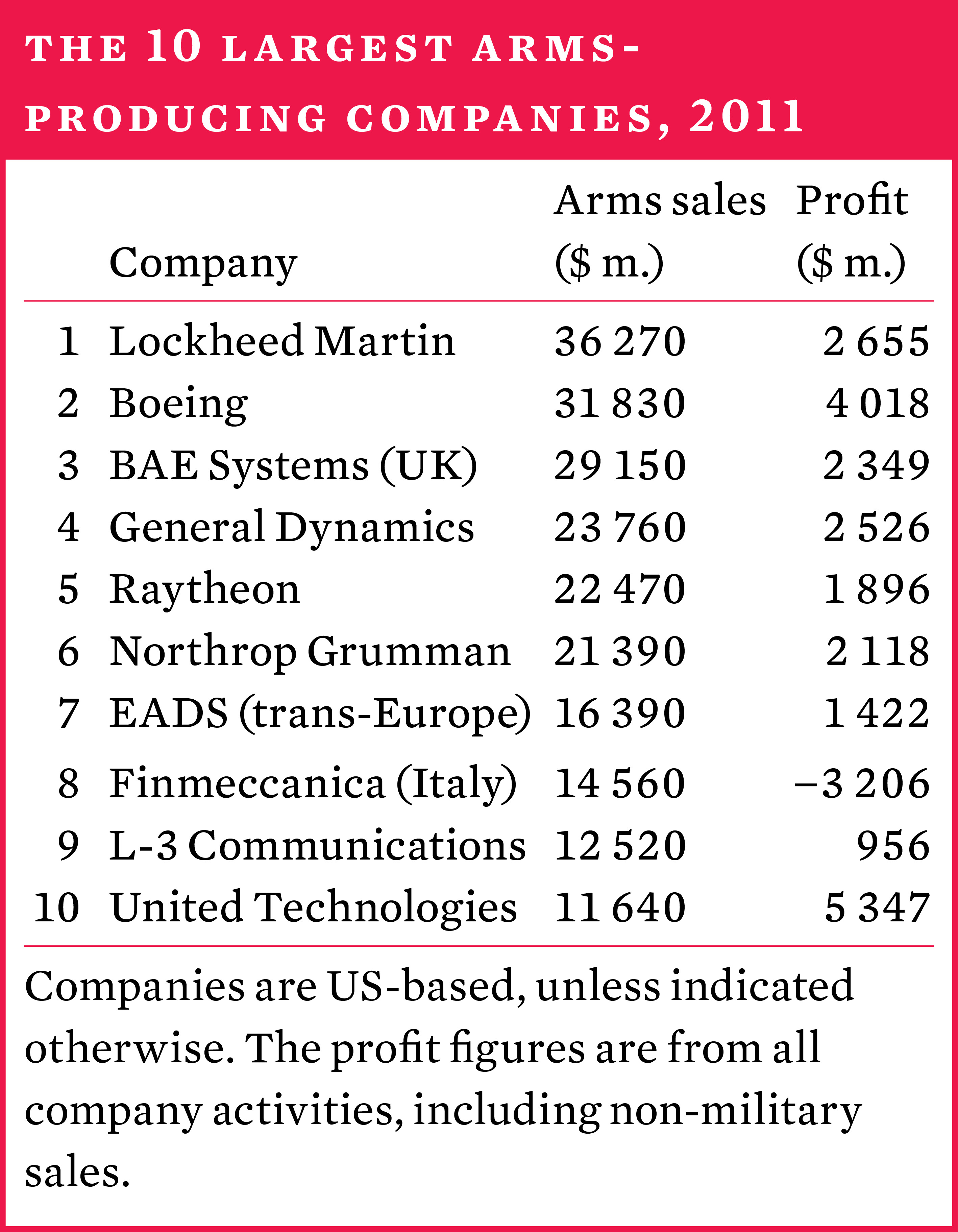

The SIPRI Top 100 arms-producing and military services companies

The SIPRI Top 100 lists the world’s 100 largest arms-producing and military services companies (excluding Chinese companies), ranked by their arms sales in 2011. Sales of arms and services by companies in the SIPRI Top 100 totalled $410 billion in 2011. In comparison with the Top 100 companies in 2010 (which is a slightly different set of companies), the 2011 arms sales represent a 5 per cent decrease in real terms.

The decrease in arms sales by the SIPRI Top 100 companies in 2011 is due to several factors, including the withdrawal from Iraq and the United Nations embargo on arms transfers to Libya; programme delays due to austerity-related military spending cuts and related postponements in weapon programme commitments; and the weak US dollar in many countries in 2011.

Associated research area

English